Whether or not you claim Missouri as your state of legal residence, there are a few things you need to be aware of this tax season since you are stationed here in the Show Me State.

A service member’s state of legal residence determines which state may tax military income. The Service Member’s Civil Relief Act (SCRA) provides that only a member’s state of legal residence may tax their military income. Other income earned by a military member within a state that isn’t their state of legal residence can be taxed by the state where they earned it. For example, a military member stationed here is Missouri, who has a state of legal residence of Virginia, and who works a second job at Wal-Mart, would have his military wages taxed by Virginia, and his wages from Wal-Mart taxed by Missouri. By default, the state from which somebody entered the armed forces is presumed to be their state of legal residence (and the military refers to this initial state as a member’s Home of Record). A member’s state of legal residence (also referred to as their domicile) may be changed to by completing a DD Form 2058 and submitting to your local finance office. See the Where to File / Where am I a Resident handout for more information on determining or changing your state of legal residence.

The Military Spouses Residency Act similarly provides that the income earned by spouses of service members cannot be taxed by a state other than the spouses state of legal residence. However, under this Act the spouse’s state of legal residence must either be (1) the same as that of their service member spouse, or (2) the state in which they are currently residing.

STATE OF LEGAL RESIDENCE OTHER THAN MISSOURI

If a military member’s state of legal residence is not Missouri, and they earned only military income, the military income is not taxed by Missouri, and the member should fill out the No Return Required-Military online form at https://sa.dor.mo.gov/nri/. During the year, Missouri runs reports detailing the names of people with addresses within the state, and who filed Federal income taxes, but did not file pay Missouri taxes. If you do not fill out this No Return Required form, you will most likely receive tax deficiency notices from the State of Missouri for not paying taxes that the state believes you owe. Save yourself the time and hassle no and submit this easy online form.

If a military member’s state of legal residence is not Missouri, but they earned more than $600 in non-military income, this income is taxable by Missouri and they must file a Missouri tax return (Form MO-1040).

Service member spouses who have state of legal residences other than Missouri, and who make more than $600 must still file a Missouri tax return (Form MO-1040), but must include verification of your state of legal residence (such as your tax return for your state of legal residence, current driver’s license, vehicle registration, or voter identification card for that state). To properly not pay Missouri tax, a Form MO-A must also be submitted, which reports both the military pay of the service member and the income of the spouse on Line 9 of Part 1 and marking the military (nonresident) block on Line 10.

STATE OF LEGAL RESIDENCE MISSOURI

If a military member’s state of legal residence is Missouri, and they were stationed here in Missouri during 2018, they are required to file a Missouri tax return (Form MO-1040). However, Missouri Revised Statutes Section 143.174 provides a deduction for military income earned as a member of the active duty component. The amount of military income should be entered on Line 16 of the Form MO-1040 to claim this deduction. However, the service member must also provide a copy of each Leave and Earnings Statement (LES) for the year to verify your entitlement to this deduction. Failing to do this may lead to denial of this deduction. This deduction is not allowed for either state active duty, or inactive duty training.

Similarly, the military pension of military retirees who reside in Missouri is taxable in Missouri, but there is a deduction. Retirees therefore need to file a Form MO-1040 (claiming the pension deduction on Line 8) as well as part 3, section D, of Form MO-A.

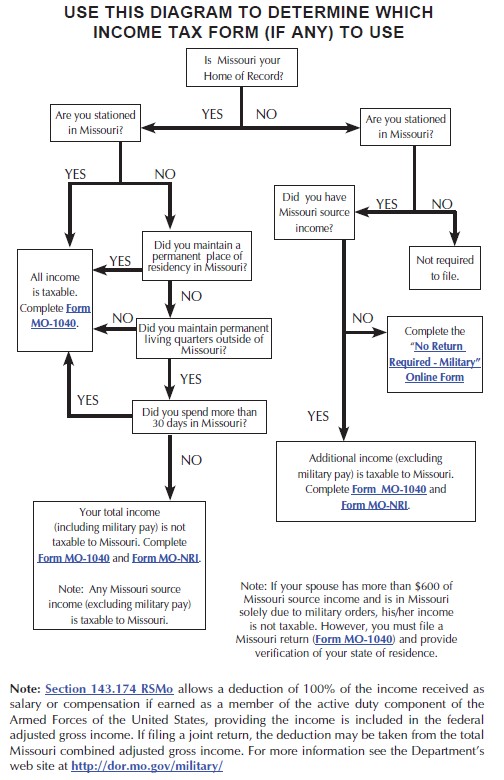

Below is an illustration provided by the Missouri Department of Revenue to help military members which form to use in Missouri. You should note, they use the term “Home of Record” to mean state of legal residence or domicile (while your Home of Record usually doesn’t change from the military’s perspective (your HOR is the location up to where the military will pay for you and your household goods to return to when you leave the military), you can change your state of legal residence/domicile during your career as discussed above).